No More Hustleporn: IPO Process and IPO Pops

Tweet by Jamin Ball

Partner at Altimeter Capital // Investing predominantly in software businesses from Series B through IPO. Dad to 2 beautiful little girls. No investment advice

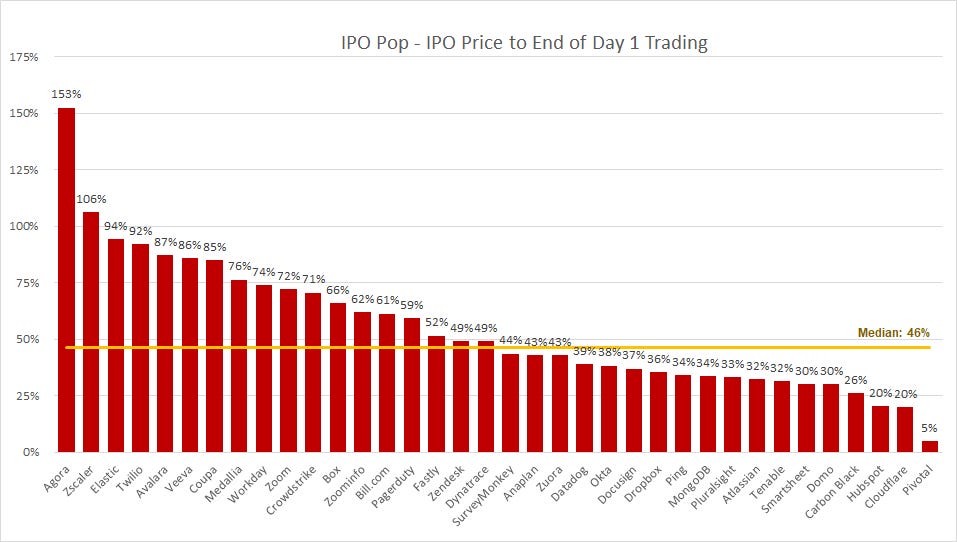

We've seen some extraordinary IPO pops recently (change in IPO price to day 1 price). nCino popped 195%, Agora popped 153%, Lemonade popped 139%, and ZoomInfo popped 62%.

Why is this happening? In my thread below I'll go over the basics of an IPO process and explain the pops 👇

An IPO process involves a company selling a large block of shares to big mutual funds and hedge funds. Typically the amount of shares they're selling represent 10-15% of the total outstanding shares, and has a total value of hundreds of millions of dollars

In order to sell this volume of stock the company goes on a two week roadshow meeting with hundreds of large institutional investors through a combination of 1:1 meetings and larger group meetings, with phone / virtual meetings in between

In each meeting the company will pitch each investor on why they should invest. This process is similar to when companies raise a Series A / Series B / Series C, etc. The difference is there's no follow up meetings, and no "data room." All of the data is in the S1

After these meetings the funds that want to invest will put in an "order." Each order is typically a limit order with two components. 1) the number of shares they want to buy and 2) the highest price at which they want to buy these shares.

All of these orders are stored in an order book. An overly simplified way to think of the order book is an excel sheet with 3 columns - firm name, desired # of shares, limit price

Each institution will generally use the initial price range the company provided to guide their limit price on their order. If the order book fills up with demand, the company may decide to raise the price range. This is quite common

At the end of the roadshow the company, along with bankers and board members, will gather in a room and decide on the IPO price (price at which shares get sold to institutional investors) and how many shares (if any) they want to allocate to each firm that placed an order

I need to stress how archaic this process is. It's incredibly manual (not done algorithmically). The only true requirement is that the company sells all the IPO shares.

To determine a price they look at the order book and try to find a price that 1) allows them to sell all the IPO shares, and 2) creates the "strongest" base of shareholders. Selecting a price above the limit order of a firm most likely means you are excluding that firm from IPO

The first issue-there are only a small number of institutional investors who are considered "strong" shareholders. A strong shareholder typically has a long term view of the company and won't dump their shares at the IPO. This drives up volatility which the company wants to avoid

These "strong" shareholders know their power! They typically all have lower limit orders leaving the company with two options: 1) Price the IPO lower and include these investors, or 2) Price the IPO higher, avoid these investors and risk higher trading volatility post IPO

I've been in the room multiple times for these pricing / allocation discussions. In many cases it really did feel like the important institutional investors were "holding the company hostage" on price

Another issue - each limit order is binary. There is only 1 price associated with it and that firm is either "in" below that price, or "out" above it. It's very hard to know where the true demand lies, and there's no time for back and forth to try and raise the limit prices

You might be wondering why it's important to have a strong base of shareholders. After an IPO, the only shares that can be traded are the IPO shares (again this is typically 10-15% of total shares). The pre-existing shares are "locked-up" meaning they can't be traded for 6 months

The amount of tradable shares is called the float, and until the lockup ends this float is quite low. This means the supply is low, and a low supply can generally lead to high volatility. If all IPO investors were to sell on day 1 it could lead to huge downward volatility

To complete this thought, it's important to have strong investors who will hold the stock and not dump right away because this *could* greatly affect the stock negatively (given the low float). Most companies typically end up pricing low to include these "anchor" investors

And this brings us to day 1 of trading. On day 1 the amount of tradable shares is quite low (the float we already talked about). Typically (and especially right now for SaaS) the demand from institutional investors who were left out of the IPO and retail investors is high

When a low supply of shares hits a high volume of demand, the shares "pop." This is just basic econ principles. But given these supply / demand dynamics these pops are more artificial and not sustainable.

An easy example to demonstrate this is nCino. SaaS companies, like nCino, are typically not profitable and are valued on a multiple of their revenue. At the end of day 1 nCino had the second highest forward revenue multiple of all SaaS companies

nCino is a great company. But does a company with 55% gross margins, negative operating margins, <50% annual growth deserve to be trading at a higher multiple (ie worth more) than companies like Datadog and Zoom who are profitable and growing >100%?? Of course not!

But this unique supply / demand dynamics drove the price up on day 1 and gave it a huge "pop." So in many ways it's unfair to scream at the bankers for "miss pricing" the IPO. We won't know the "true value" of the stock until the lock up ends and supply increase

My main point to wrap this all up - the current IPO process is broken. As you can see, the process I've laid out above is set up to allow for these pops. There's no dynamic pricing, it's manual, and point-in-time dynamics (like the current SaaS mania) are left out of the equation

When we look at nCino's IPO it was made public that the demand for the IPO was "~50x" greater than the supply of IPO shares. What does this tell me? The price range was set to low. Easy to drum up demand at low prices. And the manual way in which price ranges are set is broken

Companies are leaving too much money on the table (but again, they could never price their IPO at the "pop" price)

If you'd like to read more about the IPO process I go into all of the details in my article below (more detail than can fit in a thread!)